New Zealand’s number one cyclical problem is the threat of rising inflation accompanied by rising interest rates and its number one structural issue is a deficit of national savings leading to a build-up in its net national liabilities.

This being so, it was imperative that the authors of the 2014 Budget were aware of the need to restrict the Government’s impact on near term inflationary pressures and raise the national savings ratio.

The Government can be commended for doing both.

With domestic demand threatening to get out of hand and drive inflation higher the Reserve Bank of New Zealand (RBNZ) would have been looking to the Government to provide no further stimulus.

It delivered on this by providing a fiscal outlook that was net contractionary right through the forecast period on the back of three years of already contractionary policy.

It delivered on this by providing a fiscal outlook that was net contractionary right through the forecast period on the back of three years of already contractionary policy.

If you add earthquake related stuff, and crown entity activity, the overall impact turns temporarily stimulatory (enough to keep the RBNZ on its toes) but this is more a reflection of timing and transient issues rather than anything of significant import.

Surplus 2015

On the savings front, surpluses matter. This is what the Government is about to deliver. The first surplus since 2008 will arrive in 2015 and will get bigger thereafter.

Accordingly, crown net debt will peak next year and then fall in the following years.

The Government aims to improve the Crown’s Balance Sheet to keep net debt below 35% of GDP, reduce it to 20% by 2020 and constrain core crown expenses to 30% of GDP

The Government aims to improve the Crown’s Balance Sheet to keep net debt below 35% of GDP, reduce it to 20% by 2020 and constrain core crown expenses to 30% of GDP

It is well on track to achieve these objectives.

The Government sold this Budget in a manner that suggests it had softened its fiscal austerity while remaining responsible.

In our view, while it is responsible, the budget has no softening effect.

Modest giveaways

Core crown expenses are forecast to drop to less than 30% of GDP in fiscal 2017 from a peak of 35.1% in 2011. Based on our inflation projections, this will represent a mere 0.6% per annum increase in real expenditure over the next four years.

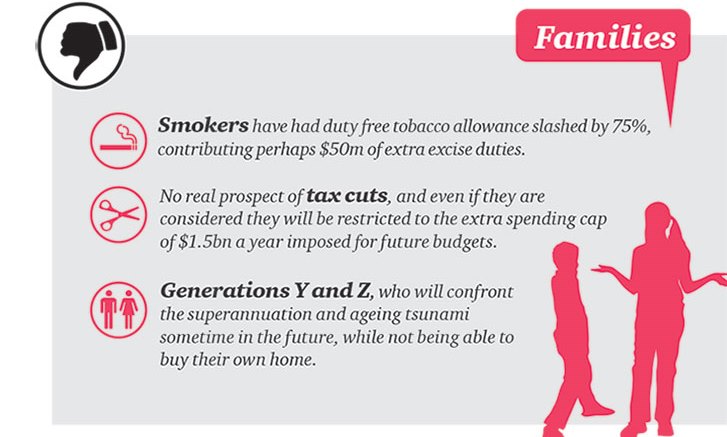

The Government need not enact draconian fiscal tightening to achieve the results. Indeed, there is no evidence of policy announcements either directed at nominal reductions in expenditure or increased taxation. In fact, there are even a few modest giveaways such as (a) four-week increase in paid parental leave to 18 weeks (b) free doctors’ visits and prescriptions for those under 13 years of age and (c) small increases in health and education expenditure.

The Government can in part get away with this because of the solid performance of the economy. The Treasury has forecast GDP growth to average 2.8% per annum over the next four years. We are not optimistic but our forecast variance is concentrated in the out-years. We reckon that the biggest risk to our own view (and that of the Treasury) is that near-term growth may surprise on the topside.

Deficit not worrying

Compositionally, our forecasts vary to the extent that we see less of a drag from net exports and slightly lower domestic demand. The net export differential is because we see a more robust export volume profile than does Treasury. Accordingly, our current account deficit profile is not as worrisome as the Treasury would have you believe.

With economic growth come increases in employment and quite likely inflation. The Treasury acknowledges that budding inflationary pressures through its forecast interest rate track which, like our own, has the cash rate peaking at over 5%.

Where we differ is in the timing of rate increases. Treasury forecasts the 90-day bank bill rate will peak at 5.3% but this does not happen until first quarter of 2018.

We are picking this peak to arrive much earlier – by end 2015.

TWI forecasts

The Treasury also projects 4.3% bill rate by the first quarter of 2015. This represents one less rate hike than our forecasts. The difference is, however easy to explain in that the Treasury has the Trade-Weighted Index (TWI) higher for a longer period than we do.

Treasury has the TWI still up at 78.4 in the first quarter of 2016, as against our forecast of 73.5. We concede that our currency forecasts have recently tended to underestimate its strength so hence would not quibble with the Treasury supposition.

Interestingly, Treasury’s Consumer Price Index (CPI) and interest rate track is predicted on the unemployment rate falling to just 4.4%. Given that the Treasury also believes that the non-inflationary rate of unemployment is 4.5% (a heroically low assumption), then inflation may yet be more of a problem that they assume.

The risks

The Treasury has pointed out several key risks to its economic outlook. These include (1) The pace and scale of the Canterbury rebuild (2) the effect of net migration on domestic demand (3) A large fall in terms of trade (4) The response of households to interest rate increases and (5) Global downside

These risks are relatively symmetric in their impact. We concur with Treasury’s concerns and we will continue to watch developments on these fronts with much interest.

BNZ is the Title Sponsor of the Indian Newslink Indian Business Awards 2014.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}